Considering debt consolidation? Understand how this strategy can potentially lower your interest rates and simplify your payments in one go. Whether it’s the right financial move depends on your unique debt landscape. This no-fluff guide delves into the smart debt consolidation, equipping you with the clarity to decide if it aligns with your fiscal goals.

Key Takeaways For Smart Debt Consolidation

- Debt consolidation simplifies financial management by combining multiple debts into one loan or balance transfer credit card, potentially with more favorable terms and lower interest rates.

- It’s crucial to thoroughly evaluate personal debts and financial goals before considering debt consolidation, taking into account factors such as credit score, loan terms, and the total interest cost.

- When choosing a debt consolidation option, compare not only interest rates but also APRs, loan terms, lender reputation, and assess the impact on credit scores and potential risks such as accumulating new debt or securing loans with collateral.

Understanding Debt Consolidation

Debt consolidation is like a conductor in an orchestra, bringing together all the disparate elements to create a harmonious symphony. It involves merging multiple debts, such as credit card balances or personal loans, into a single loan or balance transfer credit card. This new debt consolidation loan often comes with more favorable terms and lower interest rates.

The idea is simple: instead of juggling multiple debts with different interest rates and due dates, you have one loan, one payment to make each month. This not only simplifies your finances but can also save you money on interest and potentially help you pay off your debts faster if the interest rate on the new consolidation loan is lower than the combined rates on your existing debts.

What is Debt Consolidation?

Think of debt consolidation as a tool in your financial toolbox. It’s a process where you take multiple debts with different interest rates and due dates and combine them into one single loan structure. The primary goal of debt consolidation is to simplify and reduce debt payments.

This process can result in reduced monthly payments by spreading future monthly payment over an extended loan term.

Why Consider Debt Consolidation?

Why should you consider debt consolidation? First, it may lead to more favorable payoff terms, including lower interest rates and smaller monthly payments. This can be a significant advantage if you’re currently struggling with high-interest debts.

Second, consolidating debt, such as when you consolidate credit card debt, into a single loan can simplify the management of your finances by reducing the number of bills you have to keep track of each month, especially when dealing with multiple debts.

Lastly, paying off consolidated debt consistently and on time can have a positive long-term impact on your credit scores, as it demonstrates responsible debt management.

Evaluating Your Debt Situation

Before diving headfirst into smart debt consolidation, a comprehensive assessment of your debt situation is necessary. This involves understanding the benefits and risks of debt consolidation and evaluating your ability to qualify for a loan. Debt consolidation does not work the same for everyone. It is important to consider individual financial situations before pursuing this option..

Keep in mind that while debt consolidation can hasten the debt payoff by incurring less interest compared to individual loans, it comes with certain risks. For example, with secured loans, there’s the possibility of losing the collateral if the loan is not repaid as agreed. This is why some people may ask, “Do debt consolidation loans hurt my financial situation?”

Analyzing Your Debts

Begin by cataloging your current debts. Add up your current debts and calculate the combined interest rate. This will give you a clear picture of your total debt load and the amount of interest you’re currently paying.

Consider factors impacting the interest paid on loans, including the loan amount, credit score, loan term, and repayment schedule. Once you have a clear understanding of your existing debt, you can determine the best method to consolidate it, considering the total amount to be paid off, your ability to repay, and your qualification for an inexpensive loan or credit card.

Identifying Your Financial Goals

Identifying your financial goals before securing a debt consolidation loan is also of paramount importance. Why? Because it ensures that the new loan aligns with your long-term financial health. These goals should be:

- Specific

- Measurable

- Achievable

- Relevant

- Time-based (SMART)

Remember to review and adjust your financial goals annually to ensure they are still relevant and achievable despite any changes in your personal circumstances.

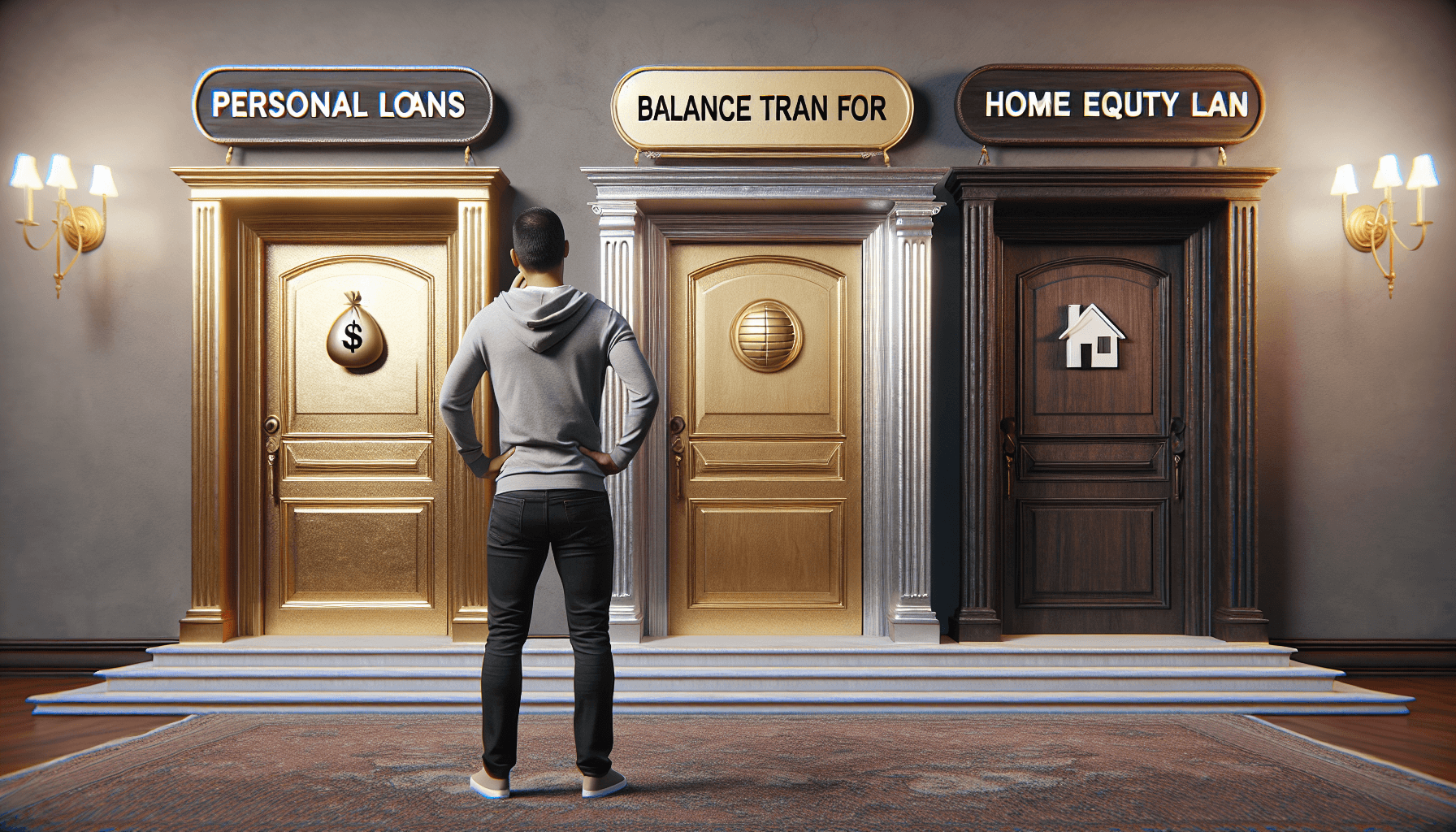

Choosing the Right Debt Consolidation Option

Having gained a clearer understanding of your debt situation and financial goals, you can now probe into your options. Smart debt consolidation methods such as personal loans, balance transfer credit cards, and home equity loans should be compared to find the most suitable one. Comparing offers from various lenders is a vital step in identifying the most suitable debt consolidation loan tailored to your specific needs.

Some lenders even offer unique benefits for debt consolidation loans, such as direct payment to creditors, rate discounts, and low credit score acceptance.

Personal Loans for Debt Consolidation

Personal loans for debt consolidation offer the following benefits:

- Lump sum payment

- Lower interest rates than credit cards

- Ideal for consolidating credit card debt

- Ability to send loan funds directly to creditors, ensuring debts are consolidated promptly.

Note that qualifying for personal loans for debt consolidation may require meeting certain criteria such as a minimum credit score, and some lenders may offer joint application options.

Balance Transfer Credit Cards

Balance transfer credit cards offer an introductory 0% APR period, typically 6 months to 2 years, for transferring existing credit card balances to help pay off debt more efficiently. However, these cards usually come with a balance transfer fee, ranging from 3% to 5% of the total amount transferred.

Transfer of balances can help in lowering credit card interest rates, however, meticulous management is essential to avoid risks such as accumulating new debt on the same card, which could offset consolidation benefits.

Home Equity Loans and Lines of Credit

Home equity loans or lines of credit can offer lower interest rates compared to credit cards or personal loans, potentially leading to significant savings over the term of the loan. However, using a home equity loan to consolidate debt introduces the risk of losing one’s home if loan payments are missed or if the loan defaults. Therefore, it’s essential to weigh the potential savings against the risks before choosing this option.

Factors to Consider When Comparing Debt Consolidation Loans

Comparison of debt consolidation loans goes beyond just finding the one with the lowest interest rate. There are several other factors to consider, such as the loan’s terms and conditions, the reputation of the lender, and the Annual Percentage Rate (APR).

Remember, a loan with a seemingly attractive interest rate might have high fees or unfavorable terms that make it less appealing in the long run.

Interest Rates and APRs

Interest rates and APRs are critical factors in debt consolidation loans as they directly influence the total cost of the loan and the potential savings when compared to original debt obligations. A borrower’s credit score is not only a crucial factor in loan approval but also determines the interest rates and APRs they are eligible for; a higher credit score typically leads to lower rates due to perceived lower risk by lenders.

Loan Terms and Monthly Payments

When comparing debt consolidation loans, the terms of the loan and monthly payments hold equal importance as the interest rates. Longer loan terms may lower monthly payments but increase the total interest paid over the life of the loan. It’s critical for borrowers to consider the total interest cost when evaluating the terms of a debt consolidation loan.

Lender Reputation and Customer Reviews

Finally, don’t forget to consider the lender’s reputation and customer reviews when comparing debt consolidation loans. A lender’s standing with the Better Business Bureau (BBB) and any complaints filed with the state attorney general can provide valuable insights.

Reading online customer reviews can also help you understand the lender’s customer service quality and the experiences of other borrowers.

The Impact of Debt Consolidation on Your Credit Score

You might be pondering, “What impact will debt consolidation have on my credit score?” as you contemplate this option. Applying for a new loan for the purpose of debt consolidation can lead to a temporary dip in your credit score due to the associated hard credit inquiry. However, over time, debt consolidation can help improve your credit score by reducing your monthly payments and credit utilization ratio, leading to a more favorable credit standing.

Short-Term Effects

In the short run, your credit scores may drop by a few points due to a hard inquiry from applying for a new loan. Opening a new credit account, such as a credit card or personal loan, temporarily lowers your credit scores as credit bureaus update your information.

The average age of credit also decreases when a new account is opened, which may lower credit scores temporarily.

Long-Term Benefits

The silver lining is that the long-term benefits of debt consolidation can outweigh these short-term effects. Payment history is the most significant factor in credit scoring, and a strong payment record on a consolidation loan can improve credit scores.

Lower credit utilization through consolidation can have a positive impact on credit scores since utilization is a key factor in credit scoring.

Common Mistakes to Avoid in Debt Consolidation

Albeit being a useful tool, debt consolidation does come with certain pitfalls. Making informed decisions can help you avoid common mistakes and ensure successful debt consolidation.

For instance, choosing a longer repayment term should be carefully considered to avoid accruing higher interest costs over the life of the loan.

Accumulating New Debt

One common mistake is accumulating new debt while consolidating existing debts. Seeing zero balances on credit cards can create an illusion of having more money, which may lead to accumulating more debt. Without addressing underlying spending behavior, taking on new debt to pay off old debt can lead to a repeating cycle of debt.

Ignoring Underlying Financial Issues

Ignoring the root causes of debt, such as habitual overspending or a lack of emergency savings, is another common mistake in debt consolidation. Successful debt consolidation should incorporate a financial plan that includes budgeting, cutting unnecessary expenses, and establishing an emergency fund.

Alternative Debt Management Strategies

Fear not, if after evaluating your financial situation, you conclude that debt consolidation isn’t the right option for you! There are other strategies to manage your debt effectively. Alternative strategies include credit counseling, the debt snowball and avalanche methods, and negotiating directly with creditors.

Debt Snowball and Avalanche Methods

The debt snowball and avalanche methods stand out as two effective strategies for paying off debts without resorting to consolidation. The snowball method focuses on paying off debts from smallest to largest balance, offering psychological wins important for staying motivated.

On the other hand, the avalanche method aims to save money over time by first eliminating debts with the highest interest rates, regardless of the balance size.

Credit Counseling and Debt Management Plans

Credit counseling services can assist individuals to better manage debt and expenses, potentially establishing a debt management plan and negotiating on their behalf.

A debt management plan (DMP) is a structured repayment plan set up and managed by a credit counseling agency where the agency negotiates with creditors to lower interest rates and create new payment terms with the goal of fully repaying debts within three to five years.

Summary

In conclusion, debt consolidation can be a valuable tool for managing and reducing debt. It involves merging multiple debts into a single loan, often with more favorable terms and lower interest rates. However, it’s important to carefully evaluate your financial situation and consider other debt management strategies. A successful debt consolidation strategy requires understanding the root causes of your debt, setting financial goals, and staying disciplined in your spending habits.

Frequently Asked Questions

Consolidating your debts is worth considering if you can secure a lower interest rate and manage the new monthly payments effectively. However, it’s important to assess your individual financial situation and credit before making a decision.

To qualify for debt consolidation, you will need good or excellent credit, a stable source of income, and possibly collateral or equity for larger loans. Lenders also consider your credit score as a sign of creditworthiness.

Yes, debt relief such as debt settlement can have a negative impact on your credit scores and may affect your ability to get credit in the future. It’s hard to predict the exact impact, as it depends on various factors.

Debt consolidation is the process of combining multiple debts into a single loan or balance transfer credit card, typically offering better terms and lower interest rates. Consider it if you have multiple debts to manage.

Debt consolidation may initially lower your credit score due to the hard inquiry, but it can improve your score in the long run by reducing your payments and credit utilization.