Lease to own home programs offer a path to homeownership for those who might not be able to buy a house outright. These programs let you rent a home while giving you the option to purchase it later. This article will explore how these programs work, their benefits, and important considerations before entering such agreements.

Key Takeaways

- Lease-to-own programs merge renting with the option to buy, making it a suitable pathway for those with low credit scores or limited savings.

- There are two primary types of lease-to-own agreements: lease option, which provides flexibility without obligation to purchase, and lease purchase, which requires commitment to buy the property at the end of the lease period.

- While lease-to-own programs can help build equity and provide stability, they may come with higher rental costs and non-refundable fees if the purchase is not completed.

0 Introduction

Lease-to-own home programs provide a promising solution for aspiring homeowners. These arrangements, merging the adaptability of renting with the long-term goal of purchasing, could be your gateway to a rent to own home. We’ll delve into the nitty-gritty of rent-to-own, from the intricacies of agreements to navigating the top rent to own program available, and even debunking common myths.

Get ready to embark on a journey to homeownership that could very well begin with a lease and end with your own set of house keys.

Understanding Lease to Own Home Programs

Starting the rent-to-own journey can be likened to embarking on a quest towards homeownership. This adventure integrates the promptness of renting with the enduring ambition of buying. But before we hoist the sails, it’s crucial to understand what a lease-to-own agreement is and how it works. It’s a unique compass in the real estate world, guiding prospective homeowners through the rent to own process of leasing a home with the option to buy it before the lease ends.

Using these programs, you can settle in a home you adore while gearing up to traverse the financial journey to outright ownership.

What is a Lease to Own Agreement?

A rent to own agreement is your ticket aboard the homeownership train, even if you’re not ready to buy a ticket outright. Rent to own agreements are versatile arrangements that allow you to rent a home while also securing a right to purchase it in the future, often with a portion of your rent contributing to the down payment.

This arrangement is particularly beneficial for those with less-than-stellar credit scores or insufficient savings, as it allows time to enhance your financial health while residing in your prospective home.

How Lease to Own Works

Once you sign on the dotted line of rent to own contracts, you commit to a voyage of monthly rent payments, with a part of that treasure potentially contributing to your future home’s purchase price. This contract is your map to eventual homeownership, detailing:

- the terms of your rental period

- the purchase option

- the final home price, which could be predetermined or based on the market value at the end of your lease.

Consider it as leasing your ideal home, with the added advantage of potential ownership, without the pressure to purchase if you’re not yet prepared.

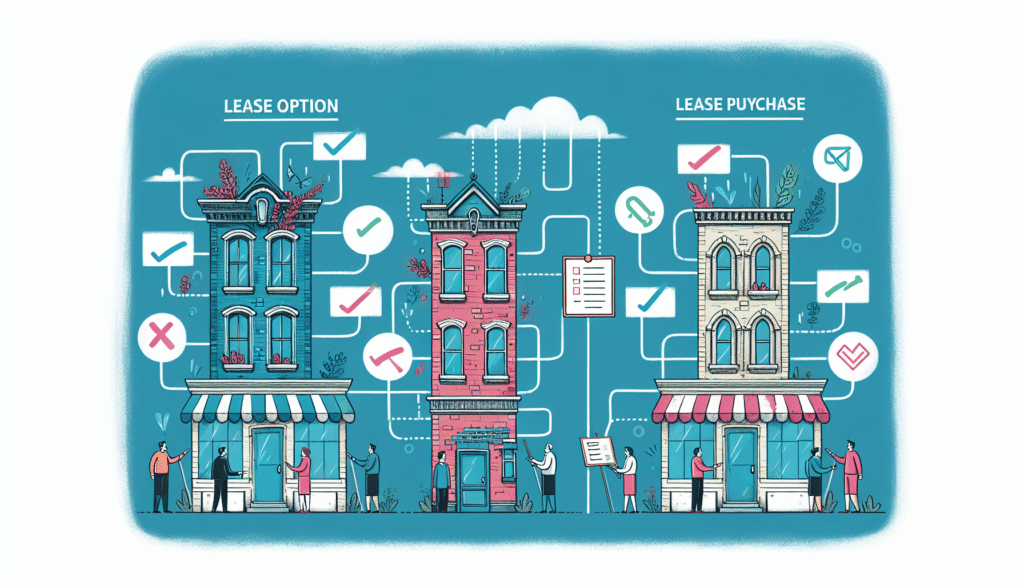

Types of Lease to Own Agreements

As you navigate through the waters of lease-to-own, you’ll encounter two main types of agreements: the lease option and the lease purchase. Like choosing between a rowboat or a sailboat, each type offers a different journey towards homeownership. The choice you make depends on your readiness to commit and your financial preparedness.

Both contracts provide the opportunity to aim for homeownership while renting, but the journey’s terms and your obligation to reach the end goal differ markedly.

Lease Option Agreement

Opting for a lease option agreement is like having a treasure map with an optional X marking the spot. You pay an upfront fee, known as the option fee, which gives you the exclusive right to buy the property when your lease concludes or during the rental period. It’s a flexible choice that gives you the freedom to decide whether to buy the property later without being legally obligated to do so.

Consider it a trial ride on your potential dream vessel, with the option to anchor it permanently in your port if it suits you.

Lease Purchase Agreement

Signing a lease purchase agreement is like committing to a voyage to undiscovered lands, with the agreement that you’ll plant your flag at the end. With this type of lease and purchase contract, you’re obligated to buy the property at the end of your lease term, no matter the seas you’ve navigated during your rental period. It requires a firm commitment and confidence in your ability to secure financing when the time comes.

This agreement caters to those with a clear financial roadmap and readiness to steer directly towards homeownership.

Comparing Lease Option and Lease Purchase Agreements

When comparing lease option and lease purchase agreements, think of it as choosing between a rental car with an option to buy and a layaway plan for your dream car. The lease option gives you the flexibility to walk away if you decide not to purchase, while the lease purchase is a binding promise to buy the vehicle at the end of the agreement.

Comprehending the differences between these two routes can align your homeownership journey with your present circumstances and future goals.

Benefits and Drawbacks of Lease to Own Programs

Navigating the seas of lease-to-own programs reveals both sunny skies and potential storms. These programs can be a lifeline for those who dream of owning a home but face financial hurdles. They offer a chance to build equity and stake a claim in a property without the immediate need for a mortgage. However, the waters can be choppy, with higher rental costs and the risk of non-refundable fees should your voyage take an unexpected turn.

It’s vital to balance the possible advantages against the disadvantages to determine if this is the suitable path for your homeownership quest.

Pros of Lease to Own Homes

The allure of lease-to-own homes lies in their ability to provide:

- Stability

- A sense of ownership from day one

- The opportunity to start building equity in your dream home

- The peace of mind that comes with knowing you won’t need to weigh anchor and move again when the rental period is up.

For those with credit scores that need polishing or savings accounts that need growing, lease-to-own homes offer the precious time needed to improve your financial standing and qualify for a mortgage. In essence, these programs can be the tide that lifts your boat, bringing you closer to the shore of homeownership.

Cons of Lease to Own Homes

However, each advantage of lease-to-own homes has a potential downside hidden below the surface. The option fees and increased monthly rents can be alluring but expensive if not handled with caution. If you’re unable to secure a mortgage at the end of the lease, these fees and any rent credits may be lost to the ocean depths.

Additionally, bearing the maintenance costs can seem like scooping water out of a sinking ship. It’s essential to consider these potential drawbacks and ensure your financial lifeboat is sturdy enough to withstand them.

Steps to Entering a Lease to Own Program

Charting a course into a lease-to-own program requires a compass of knowledge and a map of steps to follow. The journey begins with finding the right property and ends with applying for a mortgage to claim your stake in it. Along the way, you’ll:

- Negotiate the purchase price

- Sign the lease agreement

- Pay the option fee

- Make monthly rent payments

Each step is essential to guarantee a smooth journey towards homeownership and prepare you for the final phase: securing the necessary financing to permanently settle in your new home.

Finding Lease to Own Properties

Your quest for a lease-to-own property might start with a spyglass and a lookout point, searching the horizon for the right opportunity. Today’s treasure maps are online platforms and real estate agents who can help you find properties ripe for such agreements.

Don’t be afraid to present an offer to property owners directly; sometimes, they’re willing to enter a lease-to-own agreement even if their property isn’t listed as such. With tenacity and a watchful eye, you’ll discover the ideal rent to own properties to start your rent-to-own journey.

Negotiating the Purchase Price

Negotiating the home’s purchase price can be compared to bargaining in a foreign bazaar. It’s a dance between what you’re willing to pay and the home’s value. Whether the price is a fixed treasure or one that adjusts with the market’s tides at the end of your lease, it’s critical to agree upon this number before signing any contracts.

Locking in a fair price can protect you from future market swells and ensure that your investment remains a jewel worth claiming.

Signing the Lease Agreement

Inking the lease agreement is similar to marking an ‘X’ on your map. It’s a document that should clearly outline the duration of your rental period, the monthly rent, and any maintenance responsibilities that fall to you as the temporary captain of this ship.

Take the time to review these terms with a keen eye, as they dictate your rights and responsibilities while you navigate the waters of lease-to-own homeownership.

Paying the Option Fee

The option fee is your initial investment, a non-refundable amount that safeguards your right to buy the home at the lease’s end. While it may feel like a heavy chest of gold to part with, remember that this fee often ranges from 1% to 5% of the purchase price and is a necessary step in your journey. Think of it as earnest money, demonstrating your commitment to the voyage ahead.

Making Monthly Rent Payments

With the sail set, you embark on a routine of making monthly rent payments. These payments are more than just a waystation on your journey; a portion might contribute to your future ownership, like a savings account you can live in. By staying consistent with your rent payment, you’re investing in your future home.

It’s crucial to know which portion of these payments will contribute to the purchase price, as it can shape your future purchase’s financial outlook.

Applying for a Mortgage

The final leg of your lease-to-own journey involves applying for a mortgage to finance the home purchase. This step is the culmination of your efforts, where your improved credit score and saved down payment come into play.

Securing a mortgage can be a complicated process, but with adequate preparation and guidance, it can be the propelling force that lands you on the shores of homeownership.

Top Lease to Own Programs

As you aim for the horizon, it’s vital to identify which lease-to-own programs offer the most favorable conditions for your journey. Programs such as:

- Home Partners of America

- Dream America

- Divvy Homes

- Landis

offer tailored solutions to help aspiring homeowners navigate the journey with confidence. Each program has distinct features and eligibility requirements tailored to accommodate varying needs and abilities, ensuring there’s a conducive environment for every aspiring homeowner.

Home Partners of America

Home Partners of America offers a lease-to-own program that’s as steady as a lighthouse beam, guiding you through the fog of homeownership. Their program promises transparency with no hidden fees and a straightforward path to buying your home.

With requirements such as a minimum household income and clean financial history, Home Partners is an excellent option for those looking to set sail toward homeownership with a reliable crew by their side.

Dream America

Dream America’s program is like finding a treasure chest in the world of rent-to-own. They offer a 12-month lease with the flexibility to renew and eventually buy, making it an ideal choice for those who need time to get their financial ship in order.

With Dream America, you can choose your home just like you would with a traditional mortgage, ensuring that your dream home is within reach.

Divvy Homes

Divvy Homes sails into the lease-to-own seas with a clear course: a comprehensive program that includes:

- A home savings contribution

- The ability to build up your stake over time

- A significant portion of your rent going towards your future purchase every month

This makes it possible to accumulate the treasure needed for homeownership while living in the home you love.

Landis

Landis is a beacon for those navigating the complex currents of homeownership. With programs available in several states, Landis offers the support needed to make homeownership a reality. From the initial deposit to assisting with the mortgage process, Landis is there every step of the way, ensuring that the dream of owning a home is not lost in uncharted waters.

Common Misconceptions About Lease to Own

Lease-to-own programs are frequently surrounded by misconceptions and age-old stories. It’s important to realize that these programs don’t assure a purchase; they simply offer a chance to buy. Financial readiness and market conditions play significant roles in whether you’ll eventually own the home.

Additionally, while lease-to-own can be a financial lifesaver, it’s not always the treasure chest of savings some might expect, with potential risks and losses if the winds change direction and you’re unable to buy.

Avoiding Scams

Navigating the waters of lease-to-own requires a watchful eye for sirens’ calls – scams that can lead you astray. To steer clear of these treacherous waters, follow these tips:

- Verify the legitimacy of companies before entering into any lease-to-own agreement.

- Scrutinize lease terms for hidden fees or unfavorable conditions.

- Remain vigilant against deals that seem too good to be true.

By following these guidelines, you can protect yourself from potential scams and make informed decisions when considering lease-to-own options.

By taking these preventive measures, you can safeguard your homeownership journey from fraud and keep your dream of owning a home within sight.

When Lease to Own Makes Sense

Lease-to-own programs are not a universal solution; they are best suited for certain individuals navigating the path to homeownership. They are ideal for those who need time to gather the financial strength required for a traditional mortgage, like improving credit scores or amassing a down payment.

Given that a substantial number of prospective homeowners struggle to save for a down payment, lease-to-own can be the impetus that propels them ahead.

Ideal Candidates for Lease to Own

Lease-to-own programs serve as a guiding light for specific individuals on the journey to homeownership. Those who’ve weathered financial storms and need time to rebuild their credit or save for a down payment often find safe harbor in these agreements.

If you’re setting your sails toward home-buying but need a bit more time to prepare, a lease-to-own program can offer the necessary latitude to navigate your way to a mortgage and ultimately, to owning your very own home.

Situations Where Lease to Own is Advantageous

Certain circumstances make the lease-to-own route particularly advantageous. If you’re looking to anchor in a community but are still charting your financial course, these agreements offer a measure of stability. They provide a buffer to improve your credit score and gather the necessary funds for a down payment, all while living in the home you aim to buy.

In markets where home prices are rising like the tide, locking in a purchase price early can also be a smart strategy, potentially saving you from the high swell of future costs.

Key Considerations Before Signing a Lease to Own Contract

Before signing a lease-to-own contract, it’s crucial to delve into the finer details with a discerning eye. Conduct thorough research on the property, evaluate the local real estate currents, and understand every clause in your contract. These steps are like checking the hull of your ship for seaworthiness before setting sail; they ensure that your journey toward homeownership is as secure and informed as possible.

Neglecting this careful examination could leave you off course, so invest time to comprehend every facet of your lease-to-own agreement.

Researching the Property

Setting sail on a lease-to-own agreement without researching the property is like navigating without a compass. Obtain an independent appraisal to ensure the home’s value is true to market conditions, and have a detailed inspection to uncover any hidden repairs that might lurk below deck.

A title search is also critical to confirm the seller’s right to offer the home and to ensure there are no encumbrances that could snag your journey like hidden reefs.

Understanding the Terms

Grasping the terms of your lease-to-own contract is as important as understanding maritime rules. From the lease’s duration to the purchase price, every detail affects your voyage. Make sure you’re clear on maintenance responsibilities and the conditions that could lead to losing your right to purchase.

Remember, not all contracts are written in stone; they can often be adjusted to ensure fair winds and following seas throughout your agreement period.

Consulting a Real Estate Agent

Consulting an experienced real estate agent while exploring lease-to-own options can be as beneficial as having a skilled navigator on board. They can help you locate suitable properties, understand local real estate laws, and ensure that the terms of your contract are in your best interest.

A real estate attorney can further clarify your rights and obligations as a property owner, helping you to avoid potential storms and reach your destination of homeownership safely.

Summary

In the vast sea of homeownership, lease-to-own programs are a beacon for those who aren’t ready to buy outright. They offer the chance to live in and eventually buy your dream home, with a route that allows for financial preparation and credit improvement. While there are risks, like higher rents and non-refundable option fees, the potential to secure a home without a large upfront down payment is an opportunity worth considering. As with any significant voyage, the key to success is understanding the terms, navigating the process with care, and seeking guidance when needed.

Frequently Asked Questions

If you choose not to purchase the home at the end of the lease option agreement, you may lose the option fee and rent credits, but you are not obligated to buy the property and can continue renting or move on.

Yes, you can negotiate the purchase price in a lease-to-own agreement. The price is usually determined before signing the agreement and can be fixed or based on market value at the end of the lease term.

Yes, lease-to-own agreements often require an option fee, typically ranging from 1% to 5% of the home’s purchase price, which secures the right to purchase the home later. However, this fee is usually non-refundable.

To ensure a lease-to-own home program is legitimate, research the company, check reviews and ratings, verify the property’s listing on reputable platforms, review lease terms for hidden fees, and consider consulting with a real estate professional.

Before signing a lease-to-own contract, it’s important to conduct a home appraisal, schedule a property inspection, perform a title search, understand the contract terms, and consult with a real estate professional to ensure an informed decision.