You’re searching for a home, but are you ready for the critical choices ahead? Our focused guide outlines 10 things to consider home buyers like you need to deliberate before making an offer. We cover financial assessment, property selection, and more, all designed to help you navigate this significant life decision. Expect straightforward insights, ensuring a smart, prudent approach to your prospective home, without overwhelming you with premature detail.

Key Takeaways

- Before considering buying a home, individuals should evaluate their financial status, including credit score, debt-to-income ratio, and savings for down payment and closing costs, as these will influence mortgage qualification and affordability.

- The choice of property type, location, and proximity to work, schools, and amenities is critical for long-term satisfaction with the home, impacting lifestyle and resale value.

- Understanding different mortgage options and securing preapproval are essential steps in the home buying process, providing insight into budget constraints and strengthening negotiating positions with sellers.

Understanding Your Financial Status

Before embarking on your house hunting journey, you must clearly comprehend your financial status. This entails evaluating your credit score, assessing your outstanding debt, and determining your savings. For instance, your credit score significantly influences your ability to obtain a mortgage. Meanwhile, your debt level can impact your financial capacity for homeownership.

Equally important is having sufficient savings for the down payment and closing costs. Together, these personal finance topics form the foundation of your financial readiness for purchasing a home.

Credit Score: Importance and Improvement

Your credit score is a critical factor lenders consider when approving your loan, setting interest rates, and establishing loan terms. A strong credit score can open doors to favorable mortgage terms and interest rates. Regular monitoring for accuracy, reducing your credit card balances, correcting any errors on your credit report, and timely payments are effective ways to enhance your credit score.

Factors that influence your FICO score include your payment history and your credit utilization ratio, which should ideally be kept below 30 percent. Responsible debt management, prompt handling of collections, and safeguarding against identity theft are critical to maintaining high credit scores.

Evaluating Debt Payments and Income Stability

Another important aspect of your financial readiness involves evaluating your debt payments in relation to your income. Lenders use your debt-to-income ratio (DTI) to determine your loan qualification, interest rates, and loan amounts. Gaining a grasp on your DTI is fundamental in deciding how much house you can afford and sustaining financial stability post-purchase.

Taking into account your household income, monthly debts, and savings reserved for a down payment is a practical method to evaluate mortgage affordability.

Building Savings for Down Payment and Closing Costs

Building up sufficient savings for a down payment and closing costs is a key step towards homeownership. The requirement for a down payment varies depending on the loan type. Most conventional loans require a down payment of at least 3-5% of the home’s purchase price. However, FHA loans, which are insured by the Federal Housing Administration, require a minimum down payment of 3.5% and allow borrowers to use gift funds from family members to meet this requirement.

A well-thought-out savings strategy can aid in meeting these costs, paving a smoother path towards homeownership.

Property Type and Location

Selecting the suitable property type and location marks a significant milestone in the home buying process. Your current and future needs should guide your decision. This includes considering the number of stories, the existence of a basement or garage, and other living preferences that match your lifestyle.

For families with or planning to have children, selecting a location that is family-friendly and close to schools and other amenities is crucial. Let’s explore these considerations further.

Types of Properties: Single-Family, Condo, Townhouse, etc.

There are several types of properties to consider when buying a home. Each comes with its own set of advantages and disadvantages. Single-family homes, for instance, offer more privacy and space but also come with more maintenance responsibilities. Condominiums, on the other hand, might be suitable for those who prefer a community environment with shared amenities and less maintenance.

Townhouses can offer a middle ground, providing multiple floors and a small yard, with the benefits of a homeowners association (HOA) handling exterior maintenance. For those seeking a minimalist lifestyle, tiny homes can be a suitable option.

Choosing the Right Neighborhood

Your chosen neighborhood can have a significant impact on your life’s quality. Safety and low crime rates are crucial for ensuring peace of mind and maintaining or increasing property values. Amenities like parks, shopping, dining, and an active community or neighborhood association can indicate a desirable community that aligns with your lifestyle.

If you have or plan on having children, a neighborhood with a homeowners’ association (HOA), playgrounds, low traffic levels, and other children in the area can be a good choice.

Proximity to Work, Schools, and Amenities

Another important factor to consider when choosing a location is proximity to work, schools, and amenities. Living close to work can reduce commute times and lower transportation costs. The availability of public transportation options is also a key consideration, especially for those who commute or prefer sustainable travel means. With the flexibility of remote work becoming more common, housing options have expanded beyond traditional employment centers.

Having essential amenities like grocery stores, medical facilities, and entertainment venues nearby greatly enhances convenience and lifestyle.

Mortgage Options and Preapproval

Acquiring an understanding of your mortgage options and obtaining preapproval from a mortgage lender is a pivotal step in the home buying process. There are several home loan options available for first-time homebuyers, including Federal Housing Administration (FHA) loans, Veterans Affairs (VA) loans, and conventional loans.

Securing preapproval, a vital step in the home buying process, gives a clear indication of your spending capacity on a house and bolsters your negotiating position. Let’s delve deeper into these aspects.

Conventional Loans vs. FHA Loans vs. VA Loans

Understanding the differences between a conventional loan, FHA loans, and VA loans can help you make an informed decision. Conventional loans are not government-insured and may require down payments as low as 3% with good credit and reserves.

FHA loans, on the other hand, are accessible with lower credit scores and require a 3.5% down payment for a credit score of 580 or higher. The U.S. guarantees VA loans, providing support to eligible veterans and active duty members. These loans offer favorable terms and lower down payment requirements. Department of Veterans Affairs, are exclusively for individuals with VA eligibility and may offer 100% financing without a down payment.

Mortgage Interest Rates and Terms

Your debt-to-income ratio and credit score play a fundamental role in determining your interest rates and loan terms. It’s important to remember that in the initial years, your mortgage payments predominantly cover interest rather than principal, which affects equity accumulation.

The total amount you pay over the life of the loan can vary significantly depending on the interest rate, making it critical to shop around and compare mortgage rates.

The Importance of Preapproval

Obtaining preapproval is an important step in the home buying process. It not only confirms your financial credibility to sellers but also gives you a clear idea of how much you can spend on a house. Having a preapproval letter can give you a competitive edge in a hot housing market, making sellers more inclined to accept your offer.

Furthermore, knowing your preapproved loan amount allows you to target homes within your budget, thereby streamlining your search.

Working with a Real Estate Agent

Cooperating with a reliable, experienced real estate agent can considerably streamline the home buying process. A real estate agent ensures your needs and best interests are prioritized, offering market insights and helping with home identification and negotiation.

But how do you find the right real estate agent?

Finding a Trustworthy and Experienced Agent

Locating a reliable, experienced real estate agent necessitates some investigation. Start by checking their licensing and affiliations. Real estate agents must be licensed, and those affiliated with the National Association of Realtors adhere to a strict code of ethics and professional standards.

Another effective way to find potential real estate agents is through referrals from friends and colleagues. It’s also a good idea to ask prospective agents for references from recent clients.

Roles and Responsibilities of a Real Estate Agent

A real estate agent plays a crucial role in your home buying journey. Here are the different types of real estate agents you may encounter:

- Buyer’s agent: Assists buyers in finding homes, making offers, and negotiating with sellers.

- Listing agent: Helps sellers list and market their properties.

- Real estate agent with assistants: Some real estate agents operate with assistants as part of their team.

Make sure to inquire about their roles and your direct access to the agent for personal assistance.

Communicating Your Needs and Preferences

Effective communication with your real estate agent is vital for a successful home buying process. Establish a clear communication method and set reasonable expectations for response times.

Regularly provide feedback and ask questions to ensure clear and effective communication.

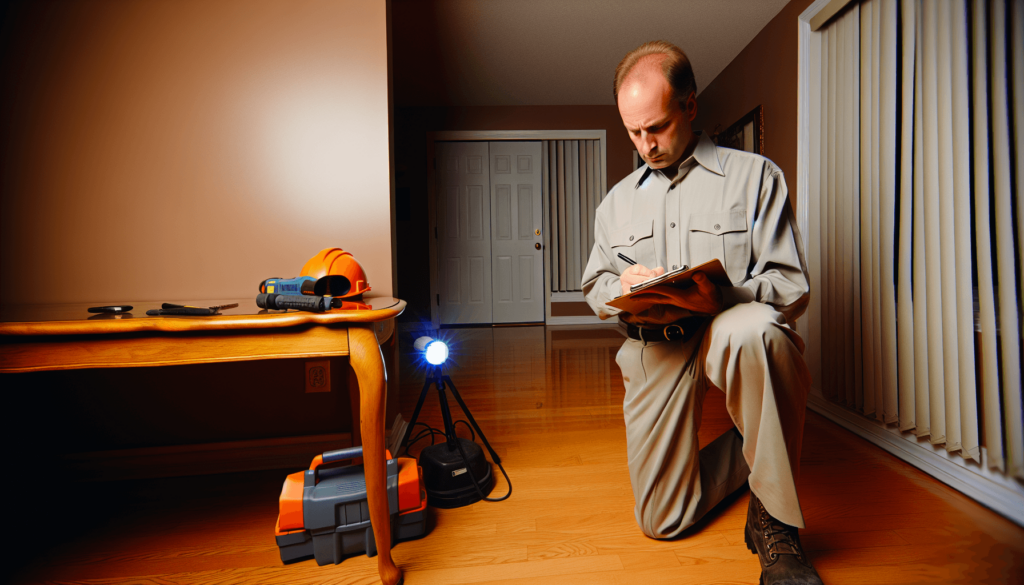

Home Inspections and Appraisals

Home inspections and appraisals are cardinal steps in the home buying process. Home inspectors perform a visual inspection of the home’s structure and main components, providing a detailed report that includes photos and descriptions of any issues found. This information can be critical in negotiating repair costs or adjusting the offer price.

Similarly, a home appraisal assesses the property’s value, which can impact your mortgage approval.

Home Inspection Process and Benefits

A thorough home inspection can reveal both existing problems and areas that may become problematic in the future, guiding your purchase decision. Standard home inspections typically examine structural elements, safety features, and systems such as plumbing and electrical.

The detailed home inspection report helps you plan for restoration and maintenance, prioritizing costs and projects.

Appraisal Process and Impact on Mortgage Approval

The appraisal process is key to understanding a home’s value and how it affects your mortgage approval. Home values are assessments of a property’s worth, typically used in the appraisal process, which are based on the prices of comparable sales in the area. Factors like the home’s age and overall condition also play substantial roles in determining its appraised value.

Addressing Issues Found During Inspections and Appraisals

Addressing issues found during home inspections and appraisals is an integral part of the home buying process. Your real estate agent can provide valuable advice and assist in action planning based on the results of the home inspection report. Home inspections typically don’t lead to mandatory repairs; instead, the decision to repair and who bears the cost is a matter for negotiation between you and the seller.

Budgeting and Affordability

Budgeting and affordability are integral aspects of the home buying process. Homeownership costs encompass not only the mortgage payment but also:

- Property taxes

- Homeowner’s insurance

- Maintenance

- Utility costs

Therefore, it’s important to factor in all these costs and maintain a financial cushion for unexpected expenses.

Factoring in Mortgage Payments, Property Taxes, and Insurance

When budgeting for homeownership, you must consider all primary monthly expenses, including the monthly payment for mortgage, property taxes, and insurance. It’s recommended that monthly mortgage payments should not surpass 28% of your income. Also, keep in mind that property tax rates depend on local municipalities and property value, and can often be deducted on federal taxes.

Home insurance costs also vary based on location and other factors, averaging around $1,200 for a standard policy.

Estimating Maintenance and Utility Costs

In addition to mortgage payments, property taxes, and insurance, it’s also important to budget for ongoing maintenance and repairs. On average, homeowners face an annual home maintenance cost of $6,548. These costs can include anything from minor repairs to major system replacements, and can significantly impact your monthly budget.

Preparing for Unexpected Expenses

Preparing for unexpected expenses is an essential part of homeownership. It’s recommended to start an emergency fund to handle unexpected financial events like medical bills or home repairs. Begin building an emergency fund with a smaller, achievable goal such as saving the equivalent of one paycheck, then aim for a buffer that covers 3 to 6 months of essentials.

This financial cushion can help you maintain homeownership without compromising your financial stability.

Negotiating and Making an Offer

Upon finding your dream home, the time to negotiate and propose an offer arrives. A real estate agent plays a critical role in this process by ensuring that your needs are met and guiding you on making a competitive offer within budget.

It’s also important to know the conditions that will allow you to back out of the purchase if necessary, before you begin shopping.

Understanding Market Conditions

Understanding local market dynamics can dictate how aggressively you should negotiate and what terms may appeal to sellers. A buyer’s market presents more houses for sale than there are buyers, often resulting in lower prices and giving buyers negotiation leverage.

On the other hand, a buyer’s market is characterized by more homes than the number of buyers, while a seller’s market is characterized by fewer homes than the number of buyers, often leading to bidding wars and properties selling quickly at higher prices.

Strategies for Successful Negotiation

Successful negotiation involves a combination of strategic offers, patience, and the courage to negotiate on various aspects such as repair costs or closing fees. During negotiations, maintain a positive demeanor, opt for in-person or phone conversations to read emotions, and use affirming language to influence the outcome in your favor.

However, always be prepared to walk away from negotiations if the deal does not meet your best interests.

Crafting a Strong Offer

Crafting a strong offer involves more than just settling on a price. Consider other terms and conditions such as:

- the timing for the transaction

- whether to include appliances or other inclusions

- in a competitive market, consider increasing the earnest money deposit or incorporating an escalation clause, while ensuring a maximum limit is set.

A personal connection or story can also help your offer stand out and gain favor.

Preparing for Closing

The closing process signifies the final step in a real estate transaction, where you formally assume ownership of the home. It involves signing a significant amount of paperwork to finalize the deal, paying closing costs, and receiving the keys to your new home.

But what should you expect during this process?

What to Expect During Closing

At closing, you will need to sign a variety of important documents that can total upwards of 100 pages. These documents include:

- Loan estimate

- Closing disclosure

- Initial escrow statement

- Mortgage note

- Deed of trust

- Certificate of occupancy for new constructions

Closing often occurs in steps and can be scheduled on different days, with a fast closing being emphasized for first-time home buyers to facilitate a smoother purchase process.

Reviewing and Signing Documents

Reviewing and signing documents at closing is a critical step in the home buying process. You will receive and sign a variety of important documents, including:

- Loan estimate

- Closing disclosure

- Initial escrow statement

- Mortgage note

- Deed of trust

- Certificate of occupancy for new constructions

It’s important to thoroughly review these documents and ensure you understand all the terms before signing.

Handling Closing Costs and Fees

Closing costs are an important part of the home buying process. These costs, which include:

- Origination

- Underwriting

- Appraisal

- Title search

- Recording

- Transfer taxes

can range between 2% to 5% of the home’s purchase price. These costs are typically paid on the actual closing day, and you should expect a precise dollar amount in the closing disclosure three days before closing.

Some costs, such as lender and rate lock fees, are negotiable, while others, such as taxes and recording fees, are non-negotiable.

Long-Term Considerations

Acquiring a home is a long-term commitment, requiring consideration of several factors beyond the initial purchase. You should consider the potential for equity growth in the property, which can significantly impact your financial security in the long term. Also, consider how the home can adapt to future life changes such as family expansion or downsizing.

Lastly, the stability and growth of the local job market can influence the future value of your home.

Future Life Changes and Home Adaptability

As life changes, so too can your housing needs. Changes in family dynamics, such as marriage, childbirth, or divorce, may require additional space or a reduction in the size of the home to better suit the new circumstances. Likewise, the onset of health concerns may result in the need for a residence with enhanced accessibility.

When choosing a home, consider its adaptability for future renovations or expansions.

Resale Value and Equity Growth

The potential resale value and equity growth of a property are important considerations when purchasing a home. Some factors that can significantly enhance a home’s future resale value include:

- Good schools in the neighborhood

- Desirable amenities and attractions nearby

- Low crime rates and a safe community

- Access to public transportation and major highways

- Upcoming development and improvements in the area

Assessing local market trends and home values prior to purchase is crucial for understanding potential equity growth and the home’s resale value.

When considering a property that requires work, it is essential to discuss with a real estate agent whether home values in the area are appreciating and the trajectory of the neighborhood’s development.

Impact of Local Economy and Job Market

The local economy and job market can have a significant impact on the value of a property. Here are some ways they can affect home sales:

- High local employment rates can increase home sales in the area.

- A struggling job market can lead to stagnation or decline in home sales.

- Potential homebuyers may delay purchases or look for homes in regions with more robust employment opportunities.

It’s also beneficial to research planned infrastructure and commercial projects in the area, as they may affect future property values.

Summary

In conclusion, buying a home is a significant financial decision that requires careful planning and informed decision-making. From understanding your financial status and selecting the right property type and location, to negotiating and making an offer, each step of the home buying process plays a vital role in ensuring a successful purchase. Also, remember to consider long-term factors such as future life changes, resale value, and the impact of the local economy and job market. With these insights, you’re now better equipped to navigate the complexities of the home buying process and make informed decisions that lead to a rewarding homeownership journey.

Frequently Asked Questions

When buying a house, focus on the price, location, house size, property taxes, and homeowners association (HOA) to make an informed decision. These factors play a crucial role in finding the right home for you.

To purchase a home, follow these 10 steps to homeownership.

Before buying a home, you should be aware of the neighborhood, property condition, and budget. These factors will help you make an informed decision.

When assessing your financial status for homeownership, consider your credit score, outstanding debts, and savings. These factors are critical for lenders’ loan approval and understanding your financial capacity for homeownership. Having sufficient savings for a down payment and closing costs is crucial.

To find a trustworthy and experienced real estate agent, start by checking their licensing and affiliations. Ask for referrals from friends and colleagues or request references from prospective agents’ recent clients.